So the blog has bee a bit quiet lately but I promise I have a few meaty posts which I have been working on. In my typical fashion I will most likely post them in rapid succession. Anyway on to this mornings post… Yesterday I read a fairly well know storage analyst’s take on the royal a$$ pounding that VMware has been taking over the past few days.

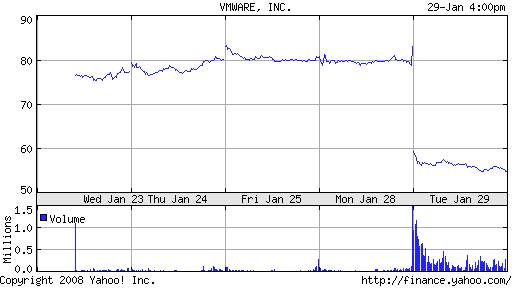

This analyst points out a number of good points like while VMW missed the top line revenue goal by only 10 million dollars they increased revenue by 80% and grew profit margins. This particular analyst takes the position of screw the street, CEO should ignore the street and just run their business. While I enjoy the idealism, let’s face it when the company went public (a choice they freely made) they relinquished control and the ultimate destiny of their company to the street, running the company has now morphed from building great products to keeping the street happy, a very different paradigm for VMW I am sure. From a different perspective I agree with the public flogging that VMW has been taking, this virtualization market while hot is still in it’s embryonic stage with < 5% of the servers in the market virtualized. VMW by no means owns the market, there is still plenty of green field. So, if I am looking at the market and companies like Microsoft and Citrix are targeting VMW doing business is going to get harder not easier. With > 95% of the market up for grabs and Microsoft’s already dominant OS position how hard do we really believe it is going to be for the "market leader" in this space. There is no doubt this is a land grab which means that VMware needs to grow top line revenues (which BTW I understand that they did by 80%) to demonstrate to the street that they are widening the gap. A companies valuation is all about the streets perception of this companies value in the future. IMO VMware has enjoyed a overly inflated valuation based on their present day value and market hype, their value in the future will be greatly diminished as players like Microsoft and Citrix truly compete for this business. At ~ 54 with a P/E of ~109 I think the price correction will continue.